Financial Statements for Non-Accountants

If you’re not an accountant, financial statements can be tough to decipher. But, they’re essential for business owners to understand since financial statements provide insights into your company’s financial health. If you can read a recipe or understand the odds of winning the lottery, you can learn to read a financial statement. Let’s start with reviewing the basic terms and aspects of financial statements.

Types of Financial Statements

There are three main types of financial statements:

- Balance Sheet – A snapshot of balances at a given point in time

- Income Statement – Shows an accumulation of transactions over a given period of time (month, quarter, year)

- Statement of Cash Flows – Shows the company’s use of cash over a given period of time (month, quarter, year)

Balance Sheet Basics

As mentioned, the balance sheet gives a glimpse of your financial position at a certain point in time. It is called a balance sheet because it shows how the total assets equal liabilities and equity (assets = liabilities + equity).

The balance sheet is broken down as follows:

- Assets – What you own (ex: cash, accounts receivable, inventory, fixed assets)

- Liabilities – What you owe (ex: accounts payable, credit cards payable, loans payable)

- Equity – Ownership stake (ex: stock, initial investment/owners’ contribution, owners’ draw, retained earnings)

What Does It All Mean?

I bet you’re thinking, “Great, thanks for the definition. But what does it all mean to me?” Let’s take a look at a sample balance sheet.

Our example company is a fitness studio that provides fitness services and sells fitness merchandise. Let’s call our company Smiles & Squats Fitness Studio. They have been in business for two years and operate in one location. We’ll analyze the balance sheet as of February 29, 2024.

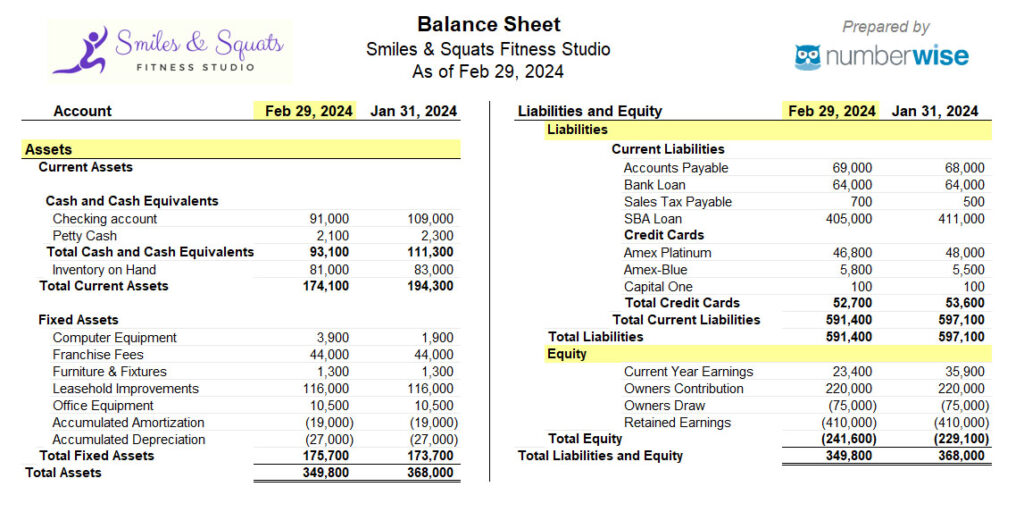

Sample Balance Sheet for Fitness Studio

Analyzing the Sample Balance Sheet

At first glance, we can see that total cash has decreased from the prior month by $18,200. This doesn’t necessarily mean that net profit has decreased.

Looking at the other sections shows that they purchased $2,000 of computer equipment, they paid $6,000 on the SBA loan, and paid $900 towards the credit card balances. You’ll also see that the sales tax payable has increased from $500 the previous month to $700.

Moving down the balance sheet, you’ll notice a decrease in inventory on hand of $2,000 from the prior month. This means they used/sold $2,000 more in inventory than they purchased during the month.

With the exception of the $2,000 addition to computer equipment, total fixed assets are the same as last month.

Bottom Line

The balance sheet doesn’t give you the entire view of this fitness studio’s finances. It doesn’t show how they are doing compared to last year, their financial projections, or the key performance indicators (KPIs) that are important to them (such as member retention, visitors per month, etc.). However, the balance sheet is a helpful snapshot of a certain point in time.

Stay tuned for upcoming blogs on understanding financial statements, where we’ll break down the income statement and cash flow statement.